On Path Independence

2017 Jun 22

See all posts

On Path Independence

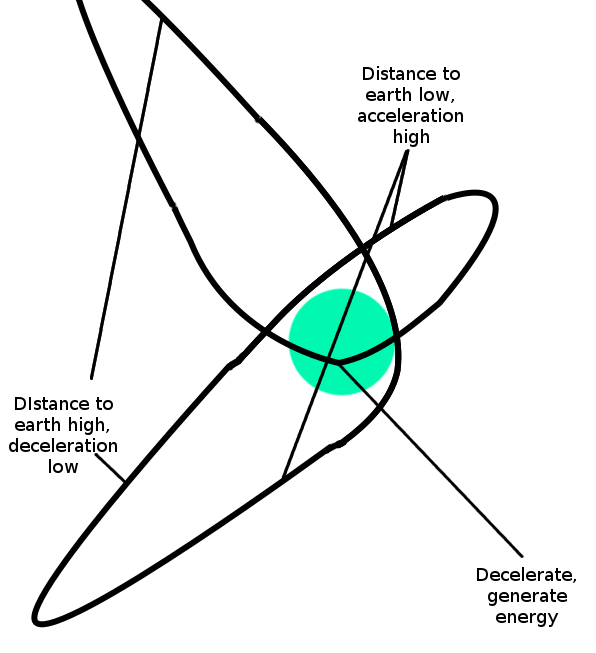

Suppose that someone walks up to you and starts exclaiming to you that he thinks he has figured out how to create a source of unlimited free energy. His scheme looks as follows. First, you get a spaceship up to low Earth orbit. There, Earth's gravity is fairly high, and so the spaceship will start to accelerate heavily toward the earth. The spaceship puts itself into a trajectory so that it barely brushes past the Earth's atmosphere, and then keeps hurtling far into space. Further in space, the gravity is lower, and so the spaceship can go higher before it starts once again coming down. When it comes down, it takes a curved path toward the Earth, so as to maximize its time in low orbit, maximizing the acceleration it gets from the high gravity there, so that after it passes by the Earth it goes even higher. After it goes high enough, it flies through the Earth's atmosphere, slowing itself down but using the waste heat to power a thermal reactor. Then, it would go back to step one and keep going.

Something like this:

Now, if you know anything about Newtonian dynamics, chances are you'll immediately recognize that this scheme is total bollocks. But how do you know? You could make an appeal to symmetry, saying "look, for every slice of the orbital path where you say gravity gives you high acceleration, there's a corresponding slice of the orbital path where gravity gives you just as high deceleration, so I don't see where the net gains are coming from". But then, suppose the man presses you. "Ah," he says, "but in that slice where there is high acceleration your initial velocity is low, and so you spend a lot of time inside of it, whereas in the corresponding slice, your incoming velocity is high, and so you have less time to decelerate". How do you really, conclusively, prove him wrong?

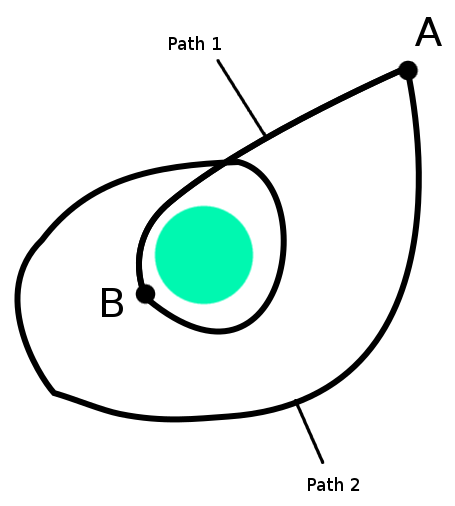

One approach is to dig deeply into the math, calculate the integrals, and show that the supposed net gains are in fact exactly equal to zero. But there is also a simple approach: recognize that energy is path-independent. That is, when the spaceship moves from point \(A\) to point \(B\), where point \(B\) is closer to the earth, its kinetic energy certainly goes up because its speed increases. But because total energy (kinetic plus potential) is conserved, and potential energy is only dependent on the spaceship's position, and not how it got there, we know that regardless of what path from point \(A\) to point \(B\) the spaceship takes, once it gets to point \(B\) the total change in kinetic energy will be exactly the same.

Different paths, same change in energy

Furthermore, we know that the kinetic energy gain from going from point \(A\) to point \(A\) is also independent of the path you take along the way: in all cases it's exactly zero.

One concern sometimes cited against on-chain market makers (that is, fully automated on-chain mechanisms that act as always-available counterparties for people who wish to trade one type of token for another) is that they are invariably easy to exploit.

As an example, let me quote a recent post discussing this issue in the context of Bancor:

The prices that Bancor offers for tokens have nothing to do with the actual market equilibrium. Bancor will always trail the market, and in doing so, will bleed its reserves. A simple thought experiment suffices to illustrate the problem. Suppose that market panic sets around X. Unfounded news about your system overtake social media. Let's suppose that people got convinced that your CEO has absconded to a remote island with no extradition treaty, that your CFO has been embezzling money, and your CTO was buying drugs from the darknet markets and shipping them to his work address to make a Scarface-like mound of white powder on his desk. Worse, let's suppose that you know these allegations to be false. They were spread by a troll army wielded by a company with no products, whose business plan is to block everyone's coin stream. Bancor would offer ever decreasing prices for X coins during a bank run, until it has no reserves left. You'd watch the market panic take hold and eat away your reserves. Recall that people are convinced that the true value of X is 0 in this scenario, and the Bancor formula is guaranteed to offer a price above that. So your entire reserve would be gone.

The post discusses many issues around the Bancor protocol, including details such as code quality, and I will not touch on any of those; instead, I will focus purely on the topic of on-chain market maker efficiency and exploitability, using Bancor (along with MKR) purely as examples and not seeing to make any judgements on the quality of either project as a whole.

For many classes of naively designed on-chain market makers, the comment above about exploitability and trailing markets applies verbatim, and quite seriously so. However, there are also classes of on-chain market makers that are definitely not suspect to their entire reserve being drained due to some kind of money-pumping attack. To take a simple example, consider the market maker selling MKR for ETH whose internal state consists of a current price, \(p\), and which is willing to buy or sell an infinitesimal amount of MKR at each price level. For example, suppose that \(p = 5\), and you wanted to buy 2 MKR. The market would sell you:

- 0.00...01 MKR at a price of 5 ETH/MKR

- 0.00...01 MKR at a price of 5.00...01 ETH/MKR

- 0.00...01 MKR at a price of 5.00...02 ETH/MKR

- ....

- 0.00...01 MKR at a price of 6.99...98 ETH/MKR

- 0.00...01 MKR at a price of 6.99...99 ETH/MKR

Altogether, it's selling you 2 MKR at an average price of 6 ETH/MKR (ie. total cost 12 ETH), and at the end of the operation \(p\) has increased to 7. If someone then wanted to sell 1 MKR, they would be spending 6.5 ETH, and at the end of that operation \(p\) would drop back down to 6.

Now, suppose that I told you that such a market maker started off at a price of \(p = 5\), and after an unspecified series of events \(p\) is now 4. Two questions:

- How much MKR did the market maker gain or lose?

- How much ETH did the market maker gain or lose?

The answers are: it gained 1 MKR, and lost 4.5 ETH. Notice that this result is totally independent of the path that \(p\) took. Those answers are correct if \(p\) went from 5 to 4 directly with one buyer, they're correct if there was first one buyer that took \(p\) from 5 to 4.7 and a second buyer that took \(p\) the rest of the way to 4, and they're even correct if \(p\) first dropped to 2, then increased to 9.818, then dropped again to 0.53, then finally rose again to 4.

Why is this the case? The simplest way to see this is to see that if \(p\) drops below 4 and then comes back up to 4, the sells on the way down are exactly counterbalanced by buys on the way up; each sell has a corresponding buy of the same magnitude at the exact same price. But we can also see this by viewing the market maker's core mechanism differently. Define the market maker as having a single-dimensional internal state \(p\), and having MKR and ETH balances defined by the following formulas:

\(mkr\_balance(p) = 10 - p\)

\(eth\_balance(p) = p^2/2\)

Anyone has the power to "edit" \(p\) (though only to values between 0 and 10), but they can only do so by supplying the right amount of MKR or ETH, and getting the right amount of MKR and ETH back, so that the balances still match up; that is, so that the amount of MKR and ETH held by the market maker after the operation is the amount that they are supposed to hold according to the above formulas, with the new value for \(p\) that was set. Any edit to \(p\) that does not come with MKR and ETH transactions that make the balances match up automatically fails.

Now, the fact that any series of events that drops \(p\) from 5 to 4 also raises the market maker's MKR balance by 1 and drops its ETH balance by 4.5, regardless of what series of events it was, should look elementary: \(mkr\_balance(4) - mkr\_balance(5) = 1\) and \(eth\_balance(4) - eth\_balance(5) = -4.5\).

What this means is that a "reserve bleeding" attack on a market maker that preserves this kind of path independence property is impossible. Even if some trolls successfully create a market panic that drops prices to near-zero, when the panic subsides, and prices return to their original levels, the market maker's position will be unchanged - even if both the price, and the market maker's balances, made a bunch of crazy moves in the meantime.

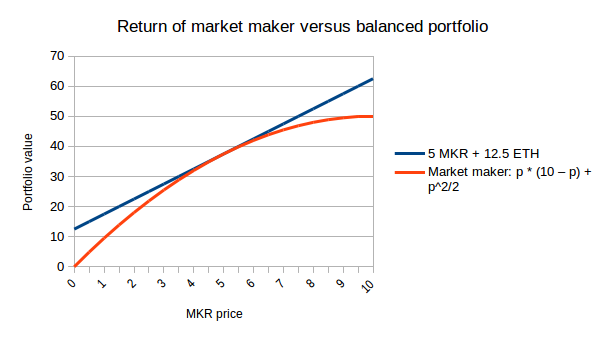

Now, this does not mean that market makers cannot lose money, compared to other holding strategies. If, when you start off, 1 MKR = 5 ETH, and then the MKR price moves, and we compare the performance of holding 5 MKR and 12.5 ETH in the market maker versus the performance of just holding the assets, the result looks like this:

Holding a balanced portfolio always wins, except in the case where prices stay exactly the same, in which case the returns of the market maker and the balanced portfolio are equal. Hence, the purpose of a market maker of this type is to subsidize guaranteed liquidity as a public good for users, serving as trader of last resort, and not to earn revenue. However, we certainly can modify the market maker to earn revenue, and quite simply: we have it charge a spread. That is, the market maker might charge \(1.005\cdot p\) for buys and offer only \(0.995\cdot p\) for sells. Now, being the beneficiary of a market maker becomes a bet: if, in the long run, prices tend to move in one direction, then the market maker loses, at least relative to what they could have gained if they had a balanced portfolio. If, on the other hand, prices tend to bounce around wildly but ultimately come back to the same point, then the market maker can earn a nice profit. This sacrifices the "path independence" property, but in such a way that any deviations from path independence are always in the market maker's favor.

There are many designs that path-independent market makers could take; if you are willing to create a token that can issue an unlimited quantity of units, then the "constant reserve ratio" mechanism (where for some constant ratio \(0 \leq r \leq 1\), the token supply is \(p^{1/r - 1}\) and the reserve size is \(r \cdot p^{1/r}\) also counts as one, provided that it is implemented correctly and path independence is not compromised by bounds and rounding errors.

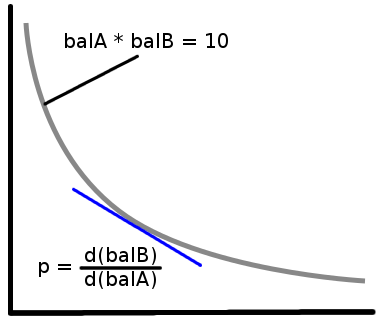

If you want to make a market maker for existing tokens without a price cap, my favorite (credit to Martin Koppelmann) mechanism is that which maintains the invariant \(tokenA\_balance(p) \cdot tokenB\_balance(p) = k\) for some constant \(k\). So the formulas would be:

\(tokenA\_balance(p) = \sqrt{k\cdot p}\)

\(tokenB\_balance(p) = \sqrt{k/p}\)

Where \(p\) is the price of \(tokenB\) denominated in \(tokenA\). In general, you can make a path-independent market maker by defining any (monotonic) relation between \(tokenA\_balance\) and \(tokenB\_balance\) and calculating its derivative at any point to give the price.

The above only discusses the role of path independence in preventing one particular type of issue: that where an attacker somehow makes a series of transactions in the context of a series of price movements in order to repeatedly drain the market maker of money. With a path independent market maker, such "money pump" vulnerabilities are impossible. However, there certainly are other kinds of inefficiencies that may exist. If the price of MKR drops from 5 ETH to 1 ETH, then the market maker used in the example above will have lost 28 ETH worth of value, whereas a balanced portfolio would only have lost 20 ETH. Where did that 8 ETH go?

In the best case, the price (that is to say, the "real" price, the price level where supply and demand among all users and traders matches up) drops quickly, and some lucky trader snaps up the deal, claiming an 8 ETH profit minus negligible transaction fees. But what if there are multiple traders? Then, if the price between block \(n\) and block \(n+1\) differs, the fact that traders can bid against each other by setting transaction fees creates an all-pay auction, with revenues going to the miner. As a consequence of the revenue equivalence theorem, we can deduce that we can expect that the transaction fees that traders send into this mechanism will keep going up until they are roughly equal to the size of the profit earned (at least initially; the real equilibrium is for miners to just snap up the money themselves). Hence, either way schemes like this are ultimately a gift to the miners.

One way to increase social welfare in such a design is to make it possible to create purchase transactions that are only worthwhile for miners to include if they actually make the purchase. That is, if the "real" price of MKR falls from 5 to 4.9, and there are 50 traders racing to arbitrage the market maker, and only the first one of those 50 will make the trade, then only that one should pay the miner a transaction fee. This way, the other 49 failed trades will not clog up the blockchain. EIP 86, slated for Metropolis, opens up a path toward standardizing such a conditional transaction fee mechanism (another good side effect is that this can also make token sales more unobtrusive, as similar all-pay-auction mechanics apply in many token sales).

Additionally, there are other inefficiencies if the market maker is the only available trading venue for tokens. For example, if two traders want to exchange a large amount, then they would need to do so via a long series of small buy and sell transactions, needlessly clogging up the blockchain. To mitigate such efficiencies, an on-chain market maker should only be one of the trading venues available, and not the only one. However, this is arguably not a large concern for protocol developers; if there ends up being a demand for a venue for facilitating large-scale trades, then someone else will likely provide it.

Furthermore, the arguments here only talk about path independence of the market maker assuming a given starting price and ending price. However, because of various psychological effects, as well as multi-equilibrium effects, the ending price is plausibly a function not just of the starting price and recent events that affect the "fundamental" value of the asset, but also of the pattern of trades that happens in response to those events. If a price-dropping event takes place, and because of poor liquidity the price of the asset drops quickly, it may end up recovering to a lower point than if more liquidity had been present in the first place. That said, this may actually be an argument in favor of subsidied market makers: if such multiplier effects exist, then they will have a positive impact on price stability that goes beyond the first-order effect of the liquidity that the market maker itself provides.

There is likely a lot of research to be done in determining exactly which path-independent market maker is optimal. There is also the possibility of hybrid semi-automated market makers that have the same guaranteed-liquidity properties, but which include some element of asynchrony, as well as the ability for the operator to "cut in line" and collect the profits in cases where large amounts of capital would otherwise be lost to miners. There is also not yet a coherent theory of just how much (if any) on-chain automated guaranteed liquidity is optimal for various objectives, and to what extent, and by whom, these market makers should be subsidized. All in all, the on-chain mechanism design space is still in its early days, and it's certainly worth much more broadly researching and exploring various options.

On Path Independence

2017 Jun 22 See all postsSuppose that someone walks up to you and starts exclaiming to you that he thinks he has figured out how to create a source of unlimited free energy. His scheme looks as follows. First, you get a spaceship up to low Earth orbit. There, Earth's gravity is fairly high, and so the spaceship will start to accelerate heavily toward the earth. The spaceship puts itself into a trajectory so that it barely brushes past the Earth's atmosphere, and then keeps hurtling far into space. Further in space, the gravity is lower, and so the spaceship can go higher before it starts once again coming down. When it comes down, it takes a curved path toward the Earth, so as to maximize its time in low orbit, maximizing the acceleration it gets from the high gravity there, so that after it passes by the Earth it goes even higher. After it goes high enough, it flies through the Earth's atmosphere, slowing itself down but using the waste heat to power a thermal reactor. Then, it would go back to step one and keep going.

Something like this:

Now, if you know anything about Newtonian dynamics, chances are you'll immediately recognize that this scheme is total bollocks. But how do you know? You could make an appeal to symmetry, saying "look, for every slice of the orbital path where you say gravity gives you high acceleration, there's a corresponding slice of the orbital path where gravity gives you just as high deceleration, so I don't see where the net gains are coming from". But then, suppose the man presses you. "Ah," he says, "but in that slice where there is high acceleration your initial velocity is low, and so you spend a lot of time inside of it, whereas in the corresponding slice, your incoming velocity is high, and so you have less time to decelerate". How do you really, conclusively, prove him wrong?

One approach is to dig deeply into the math, calculate the integrals, and show that the supposed net gains are in fact exactly equal to zero. But there is also a simple approach: recognize that energy is path-independent. That is, when the spaceship moves from point \(A\) to point \(B\), where point \(B\) is closer to the earth, its kinetic energy certainly goes up because its speed increases. But because total energy (kinetic plus potential) is conserved, and potential energy is only dependent on the spaceship's position, and not how it got there, we know that regardless of what path from point \(A\) to point \(B\) the spaceship takes, once it gets to point \(B\) the total change in kinetic energy will be exactly the same.

Different paths, same change in energy

Furthermore, we know that the kinetic energy gain from going from point \(A\) to point \(A\) is also independent of the path you take along the way: in all cases it's exactly zero.

One concern sometimes cited against on-chain market makers (that is, fully automated on-chain mechanisms that act as always-available counterparties for people who wish to trade one type of token for another) is that they are invariably easy to exploit.

As an example, let me quote a recent post discussing this issue in the context of Bancor:

The post discusses many issues around the Bancor protocol, including details such as code quality, and I will not touch on any of those; instead, I will focus purely on the topic of on-chain market maker efficiency and exploitability, using Bancor (along with MKR) purely as examples and not seeing to make any judgements on the quality of either project as a whole.

For many classes of naively designed on-chain market makers, the comment above about exploitability and trailing markets applies verbatim, and quite seriously so. However, there are also classes of on-chain market makers that are definitely not suspect to their entire reserve being drained due to some kind of money-pumping attack. To take a simple example, consider the market maker selling MKR for ETH whose internal state consists of a current price, \(p\), and which is willing to buy or sell an infinitesimal amount of MKR at each price level. For example, suppose that \(p = 5\), and you wanted to buy 2 MKR. The market would sell you:

Altogether, it's selling you 2 MKR at an average price of 6 ETH/MKR (ie. total cost 12 ETH), and at the end of the operation \(p\) has increased to 7. If someone then wanted to sell 1 MKR, they would be spending 6.5 ETH, and at the end of that operation \(p\) would drop back down to 6.

Now, suppose that I told you that such a market maker started off at a price of \(p = 5\), and after an unspecified series of events \(p\) is now 4. Two questions:

The answers are: it gained 1 MKR, and lost 4.5 ETH. Notice that this result is totally independent of the path that \(p\) took. Those answers are correct if \(p\) went from 5 to 4 directly with one buyer, they're correct if there was first one buyer that took \(p\) from 5 to 4.7 and a second buyer that took \(p\) the rest of the way to 4, and they're even correct if \(p\) first dropped to 2, then increased to 9.818, then dropped again to 0.53, then finally rose again to 4.

Why is this the case? The simplest way to see this is to see that if \(p\) drops below 4 and then comes back up to 4, the sells on the way down are exactly counterbalanced by buys on the way up; each sell has a corresponding buy of the same magnitude at the exact same price. But we can also see this by viewing the market maker's core mechanism differently. Define the market maker as having a single-dimensional internal state \(p\), and having MKR and ETH balances defined by the following formulas:

\(mkr\_balance(p) = 10 - p\)

\(eth\_balance(p) = p^2/2\)

Anyone has the power to "edit" \(p\) (though only to values between 0 and 10), but they can only do so by supplying the right amount of MKR or ETH, and getting the right amount of MKR and ETH back, so that the balances still match up; that is, so that the amount of MKR and ETH held by the market maker after the operation is the amount that they are supposed to hold according to the above formulas, with the new value for \(p\) that was set. Any edit to \(p\) that does not come with MKR and ETH transactions that make the balances match up automatically fails.

Now, the fact that any series of events that drops \(p\) from 5 to 4 also raises the market maker's MKR balance by 1 and drops its ETH balance by 4.5, regardless of what series of events it was, should look elementary: \(mkr\_balance(4) - mkr\_balance(5) = 1\) and \(eth\_balance(4) - eth\_balance(5) = -4.5\).

What this means is that a "reserve bleeding" attack on a market maker that preserves this kind of path independence property is impossible. Even if some trolls successfully create a market panic that drops prices to near-zero, when the panic subsides, and prices return to their original levels, the market maker's position will be unchanged - even if both the price, and the market maker's balances, made a bunch of crazy moves in the meantime.

Now, this does not mean that market makers cannot lose money, compared to other holding strategies. If, when you start off, 1 MKR = 5 ETH, and then the MKR price moves, and we compare the performance of holding 5 MKR and 12.5 ETH in the market maker versus the performance of just holding the assets, the result looks like this:

Holding a balanced portfolio always wins, except in the case where prices stay exactly the same, in which case the returns of the market maker and the balanced portfolio are equal. Hence, the purpose of a market maker of this type is to subsidize guaranteed liquidity as a public good for users, serving as trader of last resort, and not to earn revenue. However, we certainly can modify the market maker to earn revenue, and quite simply: we have it charge a spread. That is, the market maker might charge \(1.005\cdot p\) for buys and offer only \(0.995\cdot p\) for sells. Now, being the beneficiary of a market maker becomes a bet: if, in the long run, prices tend to move in one direction, then the market maker loses, at least relative to what they could have gained if they had a balanced portfolio. If, on the other hand, prices tend to bounce around wildly but ultimately come back to the same point, then the market maker can earn a nice profit. This sacrifices the "path independence" property, but in such a way that any deviations from path independence are always in the market maker's favor.

There are many designs that path-independent market makers could take; if you are willing to create a token that can issue an unlimited quantity of units, then the "constant reserve ratio" mechanism (where for some constant ratio \(0 \leq r \leq 1\), the token supply is \(p^{1/r - 1}\) and the reserve size is \(r \cdot p^{1/r}\) also counts as one, provided that it is implemented correctly and path independence is not compromised by bounds and rounding errors.

If you want to make a market maker for existing tokens without a price cap, my favorite (credit to Martin Koppelmann) mechanism is that which maintains the invariant \(tokenA\_balance(p) \cdot tokenB\_balance(p) = k\) for some constant \(k\). So the formulas would be:

\(tokenA\_balance(p) = \sqrt{k\cdot p}\)

\(tokenB\_balance(p) = \sqrt{k/p}\)

Where \(p\) is the price of \(tokenB\) denominated in \(tokenA\). In general, you can make a path-independent market maker by defining any (monotonic) relation between \(tokenA\_balance\) and \(tokenB\_balance\) and calculating its derivative at any point to give the price.

The above only discusses the role of path independence in preventing one particular type of issue: that where an attacker somehow makes a series of transactions in the context of a series of price movements in order to repeatedly drain the market maker of money. With a path independent market maker, such "money pump" vulnerabilities are impossible. However, there certainly are other kinds of inefficiencies that may exist. If the price of MKR drops from 5 ETH to 1 ETH, then the market maker used in the example above will have lost 28 ETH worth of value, whereas a balanced portfolio would only have lost 20 ETH. Where did that 8 ETH go?

In the best case, the price (that is to say, the "real" price, the price level where supply and demand among all users and traders matches up) drops quickly, and some lucky trader snaps up the deal, claiming an 8 ETH profit minus negligible transaction fees. But what if there are multiple traders? Then, if the price between block \(n\) and block \(n+1\) differs, the fact that traders can bid against each other by setting transaction fees creates an all-pay auction, with revenues going to the miner. As a consequence of the revenue equivalence theorem, we can deduce that we can expect that the transaction fees that traders send into this mechanism will keep going up until they are roughly equal to the size of the profit earned (at least initially; the real equilibrium is for miners to just snap up the money themselves). Hence, either way schemes like this are ultimately a gift to the miners.

One way to increase social welfare in such a design is to make it possible to create purchase transactions that are only worthwhile for miners to include if they actually make the purchase. That is, if the "real" price of MKR falls from 5 to 4.9, and there are 50 traders racing to arbitrage the market maker, and only the first one of those 50 will make the trade, then only that one should pay the miner a transaction fee. This way, the other 49 failed trades will not clog up the blockchain. EIP 86, slated for Metropolis, opens up a path toward standardizing such a conditional transaction fee mechanism (another good side effect is that this can also make token sales more unobtrusive, as similar all-pay-auction mechanics apply in many token sales).

Additionally, there are other inefficiencies if the market maker is the only available trading venue for tokens. For example, if two traders want to exchange a large amount, then they would need to do so via a long series of small buy and sell transactions, needlessly clogging up the blockchain. To mitigate such efficiencies, an on-chain market maker should only be one of the trading venues available, and not the only one. However, this is arguably not a large concern for protocol developers; if there ends up being a demand for a venue for facilitating large-scale trades, then someone else will likely provide it.

Furthermore, the arguments here only talk about path independence of the market maker assuming a given starting price and ending price. However, because of various psychological effects, as well as multi-equilibrium effects, the ending price is plausibly a function not just of the starting price and recent events that affect the "fundamental" value of the asset, but also of the pattern of trades that happens in response to those events. If a price-dropping event takes place, and because of poor liquidity the price of the asset drops quickly, it may end up recovering to a lower point than if more liquidity had been present in the first place. That said, this may actually be an argument in favor of subsidied market makers: if such multiplier effects exist, then they will have a positive impact on price stability that goes beyond the first-order effect of the liquidity that the market maker itself provides.

There is likely a lot of research to be done in determining exactly which path-independent market maker is optimal. There is also the possibility of hybrid semi-automated market makers that have the same guaranteed-liquidity properties, but which include some element of asynchrony, as well as the ability for the operator to "cut in line" and collect the profits in cases where large amounts of capital would otherwise be lost to miners. There is also not yet a coherent theory of just how much (if any) on-chain automated guaranteed liquidity is optimal for various objectives, and to what extent, and by whom, these market makers should be subsidized. All in all, the on-chain mechanism design space is still in its early days, and it's certainly worth much more broadly researching and exploring various options.